vectorbtでバックテストと最適化を行う方法

vectorbtは、Pythonのライブラリであり、金融市場におけるバックテストや分析、パラメータ最適化に役立ちます。vectorbtは、NumpyやPandasなどのPythonの一般的なライブラリと組み合わせて使用できます。

vectorbtは、高速で効率的なバックテストを実行することができ、ストラテジーの構築やポートフォリオの最適化に必要なツールを提供しています。また、多様な分析を行うことができるため、市場データに対する深い理解を得ることができます。

本記事では、ボリンジャーバンド(BB)を用いた戦略のバックテスト及び、パラメータ最適化を行います。

まず、必要なライブラリをインポートして、バックテストを行う資産のデータをダウンロードします。

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import plotly.graph_objects as go

import seaborn as sns

import vectorbt as vbt

from vectorbt.generic import nb

import yfinance as yf

symbol = 'BTC-USD'

start = '2020-01-01'

end = '2022-12-31'

data = yf.download(symbol, start=start, end=end)次に、BB戦略のトレードシグナルを生成する関数を定義します。まず、移動平均線(MA)から、 BBを計算して、ロング/ショートのエントリー/エグジットシグナルを生成します。ロングシグナルは、終値がBBを上回った場合、エグジットシグナルは、終値がMAを下回った場合、ショートシグナルは、終値がBBを下回った場合、エグジットシグナルは、終値がMAを上回った場合としています。移動平均のウィンドウとBBの幅は関数の引数として与えます。また、MAはmiddle_bandと定義しています。

def generate_signals(data, window, num_stds):

# Calculate Bollinger Bands

data['middle_band'] = data['Close'].rolling(window=window).mean()

data['upper_band'] = data['middle_band'] + num_stds * data['Close'].rolling(window=window).std()

data['lower_band'] = data['middle_band'] - num_stds * data['Close'].rolling(window=window).std()

# Long signals

long_entries = data['Close'] >= data['upper_band']

long_exits = data['Close'] <= data['middle_band']

# Short signals

short_entries = data['Close'] <= data['lower_band']

short_exits = data['Close'] >= data['middle_band']

return long_entries, long_exits, short_entries, short_exits次に、バックテストを行います。ここでは、移動平均のウィンドウを20日、BBの幅は3σとします。

# Bollinger Band parameters

window = 20

num_stds = 3

long_entries, long_exits, short_entries, short_exits = generate_signals(data, window, num_stds)

# Create an instance of Portfolio

portfolio = vbt.Portfolio.from_signals(

data['Close'],

long_entries,

long_exits,

short_entries,

short_exits,

init_cash=10000, # initial capital

fees=0.0002, # trading fees

freq='D' # daily frequency

)戦略のパフォーマンスを見てみましょう。

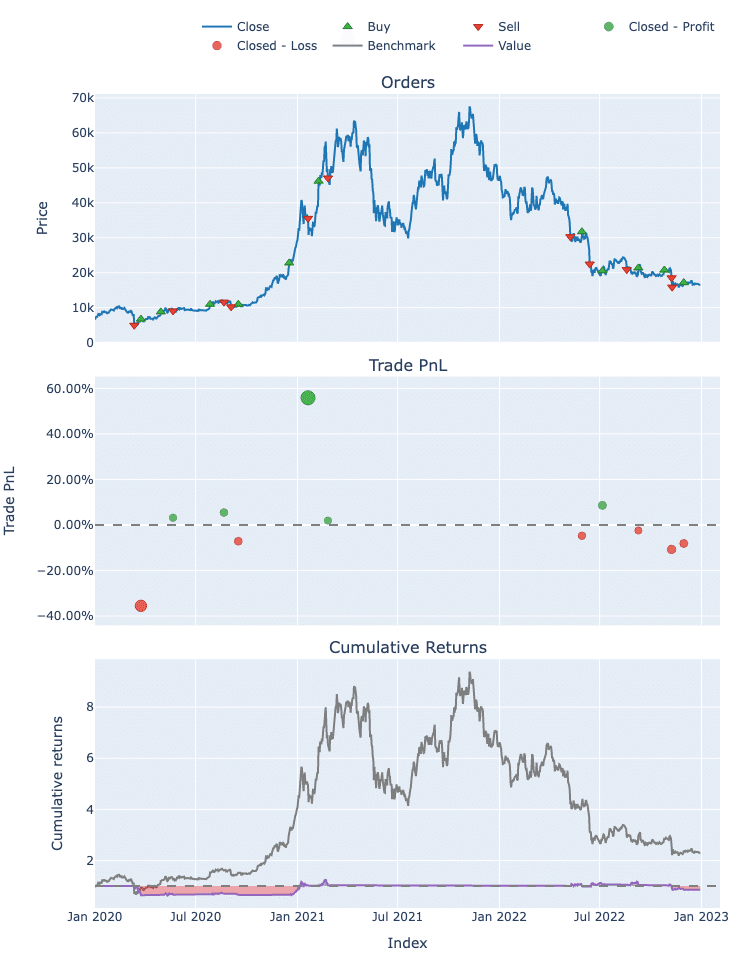

portfolio.stats()Start 2020-01-01 00:00:00

End 2022-12-30 00:00:00

Period 1095 days 00:00:00

Start Value 10000.0

End Value 8545.44632

Total Return [%] -14.545537

Benchmark Return [%] 130.585889

Max Gross Exposure [%] 100.0

Total Fees Paid 40.531792

Max Drawdown [%] 36.999794

Max Drawdown Duration 677 days 00:00:00

Total Trades 11

Total Closed Trades 11

Total Open Trades 0

Open Trade PnL 0.0

Win Rate [%] 45.454545

Best Trade [%] 55.824717

Worst Trade [%] -35.534742

Avg Winning Trade [%] 14.978711

Avg Losing Trade [%] -11.471703

Avg Winning Trade Duration 24 days 04:48:00

Avg Losing Trade Duration 16 days 20:00:00

Profit Factor 0.782565

Expectancy -132.232153

Sharpe Ratio 0.028496

Calmar Ratio -0.137964

Omega Ratio 1.009536

Sortino Ratio 0.038219

dtype: object

結果を可視化させてみましょう。

portfolio.plot().show()

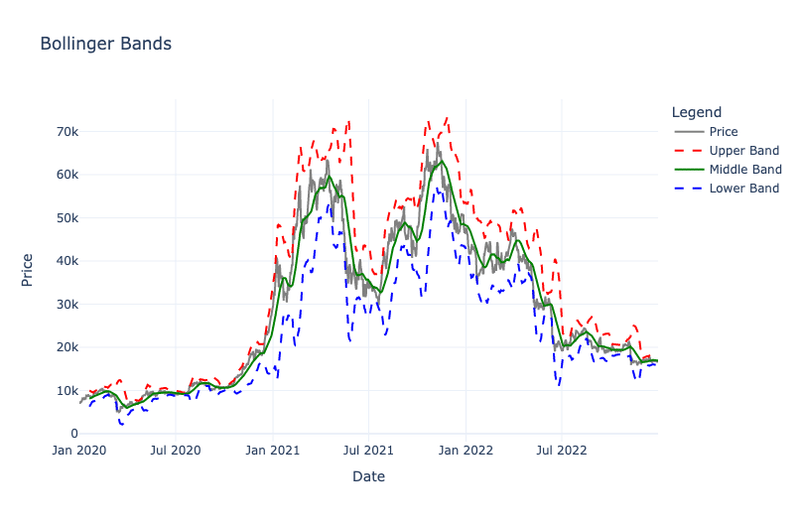

BBも可視化させてみましょう。BBと価格系列が交わるところで、ポジションの変化が行われていることを上のグラフと照らし合わせながら確認できると思います。

import plotly.graph_objects as go

# Define trace properties

trace_props = [

{'y_col': 'Close', 'name': 'Price', 'color': 'gray', 'dash': None},

{'y_col': 'upper_band', 'name': 'Upper Band', 'color': 'red', 'dash': 'dash'},

{'y_col': 'middle_band', 'name': 'Middle Band', 'color': 'green', 'dash': None},

{'y_col': 'lower_band', 'name': 'Lower Band', 'color': 'blue', 'dash': 'dash'}

]

# Create the plotly figure and add traces

fig = go.Figure([go.Scatter(x=data.index, y=data[props['y_col']], mode='lines', name=props['name'], line=dict(color=props['color'], dash=props['dash'])) for props in trace_props])

# Update the layout and show the plot

fig.update_layout(title='Bollinger Bands', xaxis_title='Date', yaxis_title='Price', legend_title='Legend', template='plotly_white').show()

次に最適化によって、最適なパラメータを探してみましょう。最適なパラメータを探した後は、その戦略を他の戦略やベンチマークと比較していきます。

まず、各パラメータでバックテストを行い、その結果をデータフレームとして返す関数を定義します。ここでは、リターン最大化をしていますが、シャープレシオ最大化なども可能です。

def optimize_strategy(data, window_range, num_stds_range):

def calc_return(window, num_stds):

long_entries, long_exits, short_entries, short_exits = generate_signals(data, window, num_stds)

portfolio = vbt.Portfolio.from_signals(

data['Close'],

long_entries,

long_exits,

short_entries,

short_exits,

init_cash=10000,

fees=0.0002,

freq='D'

)

return portfolio.total_return()

total_returns = pd.DataFrame(

data=[[calc_return(window, num_stds) for num_stds in num_stds_range] for window in window_range],

index=window_range,

columns=num_stds_range

)

return total_returns次に、複数のパラメータ候補を作成し、上の関数を実行します。

# Define the parameter ranges

window_range = np.arange(10, 61, 10)

num_stds_range = np.arange(1, 4, 0.5)

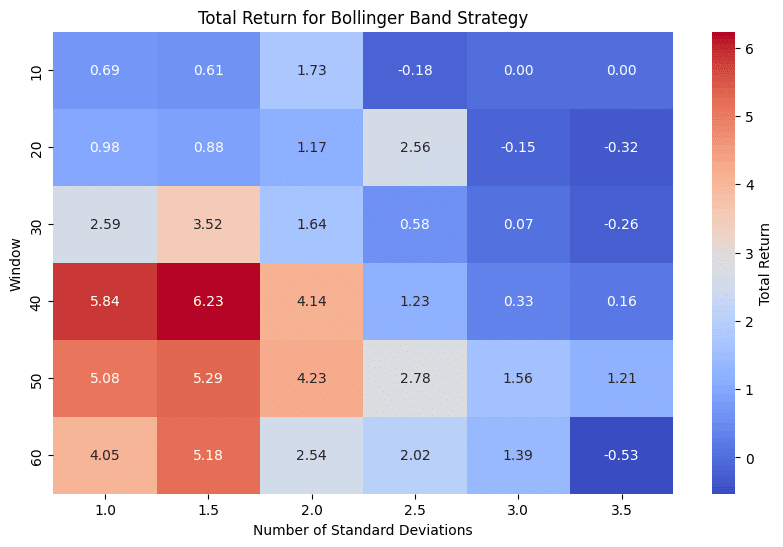

total_returns = optimize_strategy(data, window_range, num_stds_range)最もパフォーマンスの良かったパラメータの組み合わせを確認してみましょう。

max_total_return = total_returns.max().max()

best_params_idx = np.where(total_returns == max_total_return)

best_window = total_returns.index[best_params_idx[0][0]]

best_num_stds = total_returns.columns[best_params_idx[1][0]]

print(f"Best window: {best_window}")

print(f"Best number of standard deviations: {best_num_stds}")Best window: 40

Best number of standard deviations: 1.5

ヒートマップでパラメータの組み合わせを比較してみましょう。

plt.figure(figsize=(10, 6))

sns.heatmap(total_returns, annot=True, fmt='.2f', cmap='coolwarm', cbar_kws={'label': 'Total Return'})

plt.xlabel('Number of Standard Deviations')

plt.ylabel('Window')

plt.title('Total Return for Bollinger Band Strategy')

plt.show()

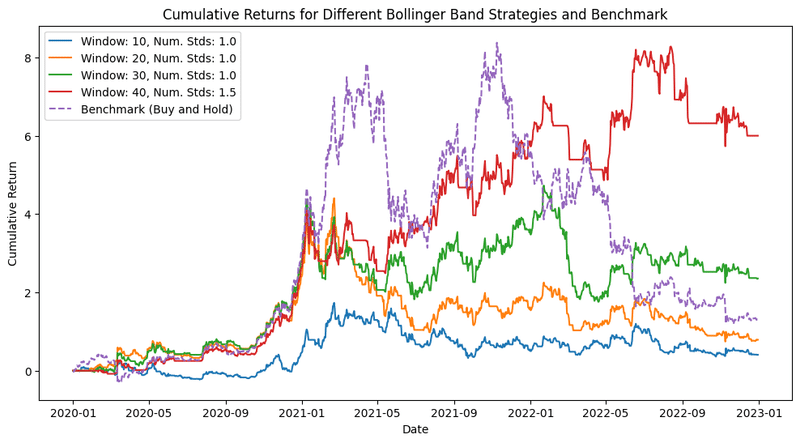

累積リターンをグラフで可視化させて、他のパラメータやベンチマークと比較してみましょう。

def cumulative_returns(data, window, num_stds):

long_entries, long_exits, short_entries, short_exits = generate_signals(data, window, num_stds)

portfolio = vbt.Portfolio.from_signals(

data['Close'],

long_entries,

long_exits,

short_entries,

short_exits,

init_cash=10000,

fees=0.001,

freq='D'

)

return portfolio.cumulative_returns()def buy_and_hold_returns(data):

portfolio = vbt.Portfolio.from_holding(data['Close'], init_cash=10000, fees=0.001, freq='D')

return portfolio.cumulative_returns()benchmark_returns = buy_and_hold_returns(data)

plt.figure(figsize=(12, 6))

params_to_compare = [

(10, 1.0),

(20, 1.0),

(30, 1.0),

(best_window, best_num_stds)

]

for params in params_to_compare:

window, num_stds = params

cum_returns = cumulative_returns(data, window, num_stds)

plt.plot(cum_returns, label=f"Window: {window}, Num. Stds: {num_stds}")

# Add the benchmark to the chart

plt.plot(benchmark_returns, label='Benchmark (Buy and Hold)', linestyle='--')

plt.xlabel('Date')

plt.ylabel('Cumulative Return')

plt.title('Cumulative Returns for Different Bollinger Band Strategies and Benchmark')

plt.legend()

plt.show()

この記事が気に入ったらサポートをしてみませんか?