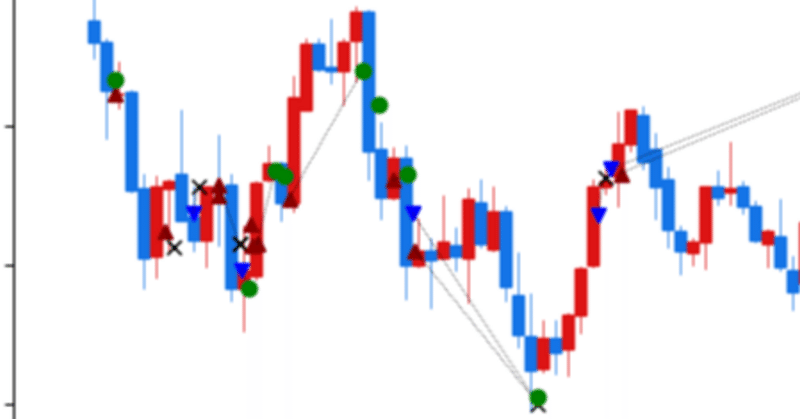

チャート上に約定履歴を表示するツールVer2(DMM FX用)

一部の業者さんでは実装されている、チャート上に約定履歴を表示するツールを作成しました。詳細は以前の記事を参照してください。

https://note.com/azk_azukisan/n/n90794f446627

前バージョンとの違い

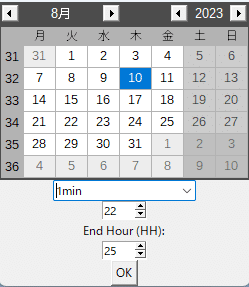

描画する時間を選択できるようになりました。

丸一日を描画すると値幅の関係でスクロールが困難だったり重かったりしたので、範囲を狭めることで動作が軽くなるようになっています。

※5分、15分足は選択できなくなりました。

OKを押すと、チャートが描画されます。

以下コード。

エディタにコピペして.pyで保存してください。

import pandas as pd

import os

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

from mpl_finance import candlestick_ohlc

import tkinter as tk

from datetime import time

from tkcalendar import Calendar

from datetime import datetime, timedelta

from tkinter import ttk

import sys

# V24 ファイルパスの設定を変更

# スクリプトがEXEとして実行されているかどうかを判定

if getattr(sys, 'frozen', False):

# EXEとして実行されている場合

application_path = os.path.dirname(sys.executable)

else:

# スクリプトとして実行されている場合

application_path = os.path.dirname(os.path.abspath(__file__))

# データファイルとトレード履歴ディレクトリのパスを設定

data_path = os.path.join(application_path, 'USDJPY_M1.csv')

trade_history_dir_path = os.path.join(application_path, 'Trade_History')

def load_trade_data(directory):

# List all csv files in the directory

files = [f for f in os.listdir(directory) if f.endswith('.csv')]

# Load each csv file and append to a list of dataframes

dfs = [pd.read_csv(os.path.join(directory, f), encoding='shift-jis') for f in files]

# Concatenate all dataframes into one

trade_data = pd.concat(dfs)

# Convert '約定日時' to datetime and set as index

trade_data['約定日時'] = pd.to_datetime(trade_data['約定日時'])

trade_data.set_index('約定日時', inplace=True)

return trade_data

def plot_ohlc_with_trades(ohlc_data, trade_data, start, end, width):

# Ensure the data is sorted by datetime

ohlc_data = ohlc_data.sort_index()

trade_data = trade_data.sort_index()

# Extract data for the given date range

data_range = ohlc_data.loc[start:end]

trade_range = trade_data.loc[start:end].copy() # Make a copy of the slice

# Prepare data for OHLC plot

ohlc = data_range[['<OPEN>', '<HIGH>', '<LOW>', '<CLOSE>']].copy()

ohlc.reset_index(inplace=True)

ohlc['Datetime'] = ohlc['Datetime'].map(mdates.date2num)

# Create plot

fig, ax = plt.subplots(figsize=(12,6))

# Plot OHLC data

candlestick_ohlc(ax, ohlc.values, width=width, colorup='#DC1414', colordown='#1474E6') # Adjusted RGB values

# Convert '決済損益(円)' to numeric

trade_range['決済損益(円)'] = trade_range['決済損益(円)'].str.replace('\\', '').str.replace(',', '').astype(float) # Remove backslash and comma, then convert to float

# Plot trades

last_buy = None

last_sell = None

for idx, row in trade_range.iterrows():

color = 'black'

marker = 'o'

if '新規' in row['区分']:

if '買' in row['売買']:

color = '#8B0000' # dark red

marker = '^'

last_buy = (idx, row['約定レート'])

elif '売' in row['売買']:

color = '#0000FF' # blue

marker = 'v'

last_sell = (idx, row['約定レート'])

elif '決済' in row['区分']:

if row['決済損益(円)'] >= 0:

color = 'green'

else:

color = 'black'

marker = 'x'

if last_buy is not None:

ax.plot([last_buy[0], idx], [last_buy[1], row['約定レート']], color='black', linestyle='dotted', linewidth=0.5) # Adjusted linewidth

last_buy = None

if last_sell is not None:

ax.plot([last_sell[0], idx], [last_sell[1], row['約定レート']], color='black', linestyle='dotted', linewidth=0.5) # Adjusted linewidth

last_sell = None

ax.plot_date(idx, row['約定レート'], fmt=' ', color=color, marker=marker) # Remove marker from fmt

# Format x-axis

ax.xaxis_date()

ax.xaxis.set_major_formatter(mdates.DateFormatter('%Y-%m-%d %H:%M'))

# Set plot title and labels

ax.set_title('OHLC Chart with Trades (Japan Time)')

ax.set_xlabel('Time')

ax.set_ylabel('Price')

# Rotate x-axis labels

plt.setp(ax.get_xticklabels(), rotation=45)

# Show plot

plt.show()

# Load MT5 OHLC data

data_path = os.path.join(application_path, 'USDJPY_M1.csv')

data = pd.read_csv(data_path, delimiter='\t') # Modify this line

data['Datetime'] = pd.to_datetime(data['<DATE>'] + ' ' + data['<TIME>'])

data['Datetime'] = data['Datetime'] + pd.Timedelta(hours=6)

data.set_index('Datetime', inplace=True)

# Load trade record data from all csv files in the specified directory

trade_history_dir_path = os.path.join(application_path, 'Trade_History')

trade_data = load_trade_data(trade_history_dir_path) # Modify this line

# Create a root window

root = tk.Tk()

# Create a calendar and a button

cal = Calendar(root)

button = tk.Button(root, text="OK", command=root.quit)

# Create a combo box for time frame selection

time_frame = ttk.Combobox(root, values=['1min'])

time_frame.current(0) # Set default value

# Pack the calendar, the combo box, and the button into the window

cal.pack()

time_frame.pack()

# Get the selected date and time frame

selected_date = cal.selection_get()

selected_time_frame = time_frame.get()

# Resample the data according to the selected time frame

if selected_time_frame == '5min':

data = data.resample('5T').agg({

'<OPEN>': 'first',

'<HIGH>': 'max',

'<LOW>': 'min',

'<CLOSE>': 'last'

})

width = 0.003

elif selected_time_frame == '15min':

data = data.resample('15T').agg({

'<OPEN>': 'first',

'<HIGH>': 'max',

'<LOW>': 'min',

'<CLOSE>': 'last'

})

width = 0.009

else:

width = 0.0006 # For 1min

start_hour = tk.Spinbox(root, from_=0, to=23, width=5)

label_end_hour = tk.Label(root, text="End Hour (HH):")

end_hour = tk.Spinbox(root, from_=0, to=23, width=5)

start_hour.pack()

label_end_hour.pack()

end_hour.pack()

button.pack()

# Run the main loop

root.mainloop()

# Get the selected date and time frame

selected_date = cal.selection_get()

selected_start_hour = int(start_hour.get())

selected_end_hour = int(end_hour.get())

# Plot the data

start = datetime.combine(selected_date, time(hour=selected_start_hour))

if selected_end_hour > 23:

selected_date += timedelta(days=1)

selected_end_hour -= 24

end = datetime.combine(selected_date, time(hour=selected_end_hour))

width = 0.00060

plot_ohlc_with_trades(data, trade_data, start, end, width)

よければ良いねとRTをお願いします…!

コードに5分15分足を書く痕跡がありますが気にしないでください…。

この記事が気に入ったらサポートをしてみませんか?