ファイナンス機械学習:分数次差分をとった特徴量:練習問題 E-mini S&P500先物ドルバー対数累積分数次差分時系列へのトリプルバー

E-mini S&P500先物ティックバーからドルバーを取り、これを対数累積した時系列を$${d=2}$$で固定ウィンドウ法で差分した定常な時系列を扱う。

hをこの分数次差分時系列の標準偏差の2倍とし、CUSUMフィルターを適用する。

import Labels as labels

dv=500_000

Dbar=bars.getDollarBars(SP_data,dv)

close = Dbar['Close'].to_frame()

logClose=np.log(close.astype(float)).cumsum()

lCFFD = fracDiff_FFD(logClose, d=2.0, thres=1e-5).dropna()

thred=lCFFD['Close'].std()

Events=bars.getTEvents(log_fd2['Close'], thred*2.)

Events

CUSUMフィルターを通したタイムスタンプをインデックスを使い、分数次差分と価格を特徴量としてData Frameに加える。

dfEvents= pd.DataFrame(index = Events).assign(Close = close,

ffd = log_fd2['Close']).drop_duplicates().dropna()トリプルバリアを、日次標準偏差の2倍の大きさの水平バリアと5日間の垂直バリアとして適用し、ラベルを作成する。

span0=20

price=dfEvents['Close']

t1 = labels.addVerticalBarrier(price, Events, numDays=5)

dfEvents['DailyVol']=labels.getDailyVol(price,span0)

dfEvents.dropna()

ptsl=[2,2]

minRet = .0002

TPevents=labels.getEventsML(dfEvents['Close'],dfEvents.index,ptsl,dfEvents['DailyVol'],minRet,t1=t1,side=None).dropna()

TPlabels=labels.getBinsTUML(TPevents,dfEvents['Close'],t1)

TPlabels = TPlabels[~(TPlabels['bin'] == 0)]

TPlabels['bin'].value_counts()

TPlabels

Sequential Bagging Classifier

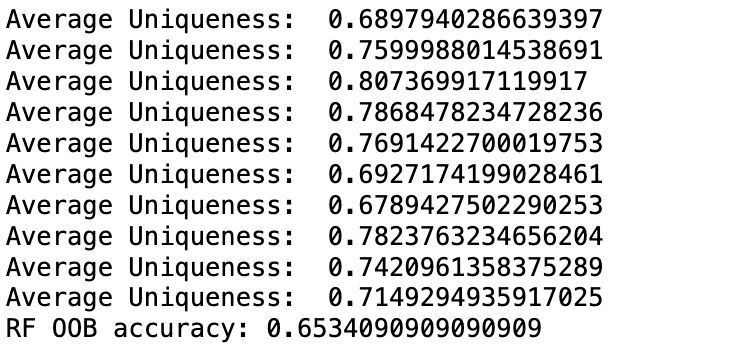

Sklearn.ensembleのBaggingClassifierを継承し、サンプルの平均独自性を計算しながらバギングを行うサンプリングを行うSequentiallyBoostrappedBaggingと、これを使用するSequentiallyBoostrappedBaggingClassifierのクラスを作成する。

import itertools

import numbers

from typing import Union

import numpy as np

import pandas as pd

from scipy import sparse

from sklearn.base import BaseEstimator

from sklearn.base import ClassifierMixin

from sklearn.ensemble import BaggingClassifier

from sklearn.ensemble._bagging import BaseBagging

from sklearn.ensemble._base import _partition_estimators

from sklearn.metrics import accuracy_score

from sklearn.tree import DecisionTreeClassifier

from sklearn.utils import check_array

from sklearn.utils import check_consistent_length

from sklearn.utils import check_random_state

from sklearn.utils import check_X_y

from sklearn.utils import indices_to_mask

from sklearn.utils._joblib import delayed

from sklearn.utils._joblib import Parallel

from sklearn.utils.random import sample_without_replacement

from sklearn.utils.validation import has_fit_parameter

from abc import ABCMeta, abstractmethod

from Weights import getIndMatrix, seqBootstrap, getAvgUniqueness

MAX_INT = np.iinfo(np.int32).max

def _generate_random_features(

random_state: np.random.RandomState,

bootstrap: bool,

n_population: int,

n_samples: int,):

if bootstrap:

indices = random_state.randint(0, n_population, n_samples)

else:

indices = sample_without_replacement(

n_population, n_samples, random_state=random_state

)

return indices

def _generate_bagging_indices(

random_state: np.random.RandomState,

bootstrap_features: bool,

n_features: int,

max_features: Union[int,float],

max_samples: Union[int,float],

indM,

):

random_state = check_random_state(random_state)

# Draw indices

feature_indices = _generate_random_features(

random_state, bootstrap_features, n_features, max_features

)

sample_indices = seqBootstrap(

pd.DataFrame(indM.toarray()), max_samples

)

print(sample_indices)

print('Average Uniqueness: ',getAvgUniqueness(pd.DataFrame(indM.toarray())[sample_indices]).mean())

return feature_indices, sample_indices

def _parallel_build_estimators(

n_estimators,

ensemble,

X,

y,

indM,

sample_weight,

seeds,

total_n_estimators,

verbose,

) :

# Retrieve settings

n_samples, n_features = X.shape

max_features = ensemble._max_features

max_samples = ensemble._max_samples

bootstrap_features = ensemble.bootstrap_features

support_sample_weight = has_fit_parameter(ensemble.estimator_, "sample_weight")

if not support_sample_weight and sample_weight is not None:

raise ValueError("The base estimator doesn't support sample weight")

# Build estimators

estimators = []

estimators_features = []

estimators_indices = []

#print('parallel build',indM)

for i in range(n_estimators):

if verbose > 1:

print(

"Building estimator %d of %d for this parallel run "

"(total %d)..." % (i + 1, n_estimators, total_n_estimators)

)

random_state = seeds[i]

estimator = ensemble._make_estimator(append=False, random_state=random_state)

# Draw random feature, sample indices

features, indices = _generate_bagging_indices(

random_state,

bootstrap_features,

n_features,

max_features,

max_samples,

indM,

)

# Draw samples, using sample weights, and then fit

if support_sample_weight:

if sample_weight is None:

curr_sample_weight = np.ones((n_samples,))

else:

curr_sample_weight = sample_weight.copy()

sample_counts = np.bincount(indices, minlength=n_samples)

curr_sample_weight *= sample_counts

estimator.fit(X[:, features], y, sample_weight=curr_sample_weight)

else:

estimator.fit((X[indices])[:, features], y[indices])

estimators.append(estimator)

estimators_features.append(features)

estimators_indices.append(indices)

return estimators, estimators_features, estimators_indices

class SequentiallyBootstrappedBaseBagging(BaseBagging, metaclass=ABCMeta):

"""

Base class for Sequentially Bootstrapped Classifier and Regressor, extension of sklearn's BaseBagging

"""

@abstractmethod

def __init__(

self,

t1:pd.Series,

estimator: BaseEstimator = None,

n_estimators: int = 10,

max_samples: Union[int, float] = 1.0,

max_features: Union[int, float] = 1.0,

bootstrap_features: bool = False,

oob_score: bool = False,

warm_start: bool = False,

n_jobs: int = None,

random_state: Union[int, np.random.RandomState, None] = None,

verbose: int = 0,

):

super().__init__(

estimator=estimator,

n_estimators=n_estimators,

bootstrap=True,

max_samples=max_samples,

max_features=max_features,

bootstrap_features=bootstrap_features,

oob_score=oob_score,

warm_start=warm_start,

n_jobs=n_jobs,

random_state=random_state,

verbose=verbose,

)

self.t1= t1

self.barIx = t1.index

self._indM = None

/

# Used for create get ind_matrix subsample during cross-validation

self.timestamp_int_index_mapping = pd.Series(

index=self.barIx, data=range(self.indM.shape[1])

)

self.X_time_index = None # Timestamp index of X_train

@property

def indM(self):

if self._indM is None:

self._indM = getIndMatrix(

self.barIx, self.t1

)

return self._indM

def fit(

self,

X: pd.DataFrame,

y: pd.Series,

sample_weight: pd.Series = None,

):

return self._fit(X, y, self.max_samples, sample_weight=sample_weight)

def _fit(

self,

X: pd.DataFrame,

y: pd.Series,

max_samples:Union[int, float] = None,

max_depth = None,

sample_weight: pd.Series = None,

):

assert isinstance(X, pd.DataFrame), "X should be a dataframe with time indices"

assert isinstance(y, pd.Series), "y should be a series with time indices"

assert isinstance(

X.index, pd.DatetimeIndex

), "X index should be a DatetimeIndex"

assert isinstance(

y.index, pd.DatetimeIndex

), "y index should be a DatetimeIndex"

random_state = check_random_state(self.random_state)

self.X_time_index = X.index # Remember X index for future sampling

set(self.X_time_index)

assert set(self.timestamp_int_index_mapping.index).issuperset(

set(self.X_time_index)

),"The ind matrix timestamps should have all the timestamps in the training data"

indM = csr_matrix(self.indM.astype(pd.SparseDtype("float64",0)).sparse.to_coo())

subsampled_indM = indM[

:, self.timestamp_int_index_mapping.loc[self.X_time_index]

]

# Convert data (X is required to be 2d and indexable)

X, y = check_X_y(

X, y, ["csr", "csc"], dtype=None, force_all_finite=False, multi_output=True

)

if sample_weight is not None:

sample_weight = check_array(sample_weight, ensure_2d=False)

check_consistent_length(y, sample_weight)

# Remap output

n_samples, self.n_features_ = X.shape

self._n_samples = n_samples

y = self._validate_y(y)

# Check parameters

self._validate_estimator()

# Validate max_samples

if not isinstance(max_samples, (numbers.Integral, np.integer)):

max_samples = int(max_samples * X.shape[0])

if not (0 < max_samples <= X.shape[0]):

raise ValueError("max_samples must be in (0, n_samples]")

# Store validated integer row sampling value

self._max_samples = max_samples

# Validate max_features

if isinstance(self.max_features, (numbers.Integral, np.integer)):

max_features = self.max_features

elif isinstance(self.max_features, float):

max_features = self.max_features * self.n_features_

else:

print(type(self.max_features))

raise ValueError("max_features must be int or float")

if not (0 < max_features <= self.n_features_):

raise ValueError("max_features must be in (0, n_features]")

max_features = max(1, int(max_features))

# Store validated integer feature sampling value

self._max_features = max_features

if self.warm_start and self.oob_score:

raise ValueError("Out of bag estimate only available if warm_start=False")

if not self.warm_start or not hasattr(self, "estimators_"):

# Free allocated memory, if anyexpiritation

self.estimators_ = []

self.estimators_features_ = []

self.sequentially_bootstrapped_samples_ = []

n_more_estimators = self.n_estimators - len(self.estimators_)

if n_more_estimators < 0:

raise ValueError(

"n_estimators=%d must be larger or equal to "

"len(estimators_)=%d when warm_start==True"

% (self.n_estimators, len(self.estimators_))

)

elif n_more_estimators == 0:

warn(

"Warm-start fitting without increasing n_estimators does not "

"fit new trees."

)

return self

# Parallel loop

n_jobs, n_estimators, starts = _partition_estimators(

n_more_estimators, self.n_jobs

)

total_n_estimators = sum(n_estimators)

# Advance random state to state after training

# the first n_estimators

if self.warm_start and len(self.estimators_) > 0:

random_state.randint(MAX_INT, size=len(self.estimators_))

seeds = random_state.randint(MAX_INT, size=n_more_estimators)

self._seeds = seeds

all_results = Parallel(n_jobs=n_jobs, verbose=self.verbose,)(

delayed(_parallel_build_estimators)(

n_estimators[i],

self,

X,

y,

subsampled_indM,

sample_weight,

seeds[starts[i] : starts[i + 1]],

total_n_estimators,

verbose=self.verbose,

)

for i in range(n_jobs)

)

# Reduce

self.estimators_ += list(

itertools.chain.from_iterable(t[0] for t in all_results)

)

self.estimators_features_ += list(

itertools.chain.from_iterable(t[1] for t in all_results)

)

self.sequentially_bootstrapped_samples_ += list(

itertools.chain.from_iterable(t[2] for t in all_results)

)

if self.oob_score:

self._set_oob_score(X, y)

self._ind_mat = None

return self

class SequentiallyBootstrappedBaggingClassifier(

SequentiallyBootstrappedBaseBagging, BaggingClassifier, ClassifierMixin

):

def __init__(

self,

t1:pd.Series,

estimator: BaseEstimator = None,

n_estimators: int = 10,

max_samples: Union[float,int] = 1.0,

max_features: Union[float, int] = 1.0,

bootstrap_features: bool = False,

oob_score: bool = False,

warm_start: bool = False,

n_jobs: int = None,

random_state: Union[int, np.random.RandomState, None]=None,

verbose: int = 0,

):

super().__init__(

t1,

estimator=estimator,

n_estimators=n_estimators,

max_samples=max_samples,

max_features=max_features,

bootstrap_features=bootstrap_features,

oob_score=oob_score,

warm_start=warm_start,

n_jobs=n_jobs,

random_state=random_state,

verbose=verbose,

)

def _validate_estimator(self):

"""

Check the estimator and set the base_estimator_ attribute.

"""

super(BaggingClassifier, self)._validate_estimator(

default=DecisionTreeClassifier()

)

def _set_oob_score(self, X: pd.DataFrame, y: pd.Series):

n_samples = y.shape[0]

n_classes_ = self.n_classes_

predictions = np.zeros((n_samples, n_classes_))

for estimator, samples, features in zip(

self.estimators_,

self.sequentially_bootstrapped_samples_,

self.estimators_features_,

):

# Create mask for OOB samples

mask = ~indices_to_mask(samples, n_samples)

if hasattr(estimator, "predict_proba"):

predictions[mask, :] += estimator.predict_proba(

(X[mask, :])[:, features]

)

else:

p = estimator.predict((X[mask, :])[:, features])

j = 0

for i in range(n_samples):

if mask[i]:

predictions[i, p[j]] += 1

j += 1

if (predictions.sum(axis=1) == 0).any():

warn(

"Some inputs do not have OOB scores. "

"This probably means too few estimators were used "

"to compute any reliable oob estimates."

)

oob_decision_function = predictions / predictions.sum(axis=1)[:, np.newaxis]

oob_score = accuracy_score(y, np.argmax(predictions, axis=1))

self.oob_decision_function_ = oob_decision_function

self.oob_score_ = oob_scoreこのファイルをインポートする。

import SeqBoostCassfier as SeqB

from sklearn.tree import DecisionTreeClassifier

from sklearn.model_selection import train_test_split

from sklearn.metrics import accuracy_score, confusion_matrix

from sklearn.metrics import precision_score, recall_score, f1_score

np.random.seed(1251)

n_estimate = 10

random_state = 42

max_samples = 50

tree = DecisionTreeClassifier(criterion='entropy',

max_depth=None,

random_state=random_state)

bagtree = SeqB.SequentiallyBootstrappedBaggingClassifier(estimator=tree,

t1=t1,

n_estimators=n_estimate,

max_samples=max_samples,

max_features=1.0,

bootstrap_features=False,

oob_score = True,

n_jobs=1,

random_state=random_state) 特徴量Xは価格時系列、対数価格累積の分数次差分時系列、日次ボラティリティとし、トリプルバリアのラベルをyとする。

トリプルバリアのラベルは、t1でのリターンに符号に一致するから、Xから抜くこととする。

X=dfEvents.drop(['bin','ret'],axis=1)

y=dfEvents['bin'].astype(int)

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.3, shuffle=False)

bag.fit(X_train,y_train)

y_pred = bagtree.predict(X_test)

y_prob = bagtree.predict_proba(X_test)[:,1]

print(f'RF OOB accuracy: {bagtree.oob_score_}')

from sklearn.metrics import classification_report

from sklearn.metrics import roc_curve,auc

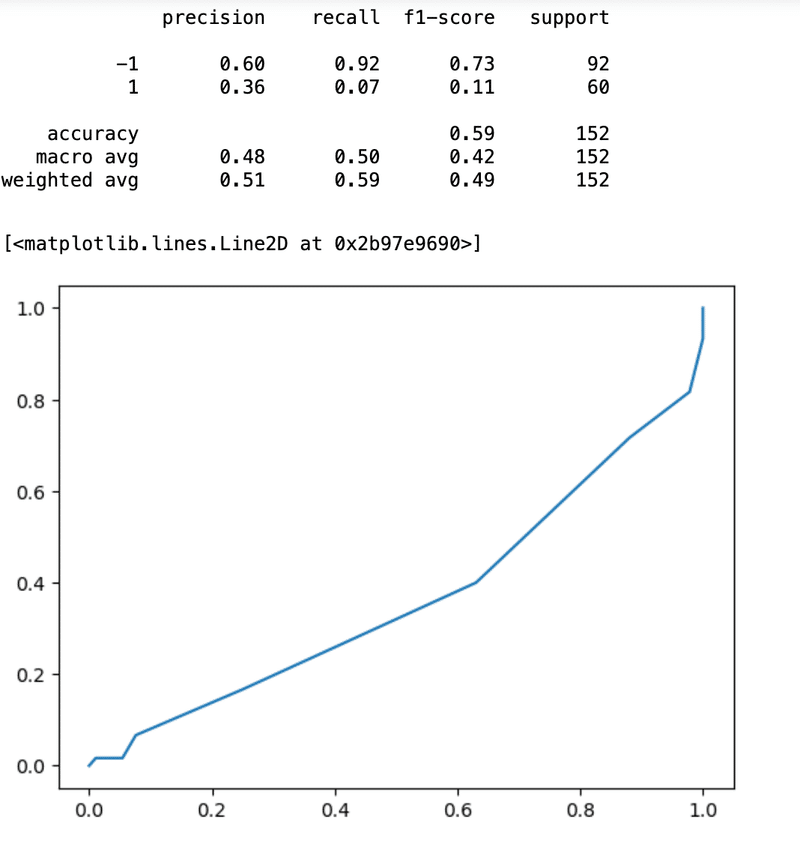

print(classification_report(y_true=y_test, y_pred=y_pred))

fpr, tpr, thresholds = roc_curve(y_test, y_prob)

roc_auc = auc(fpr, tpr)

plt.plot(fpr,tpr,label=' ROC area = %0.2f' %(roc_auc))

この記事が気に入ったらサポートをしてみませんか?