【順序プロビットモデルの導入🌟】『Japanese Foreign Exchange Interventions, 1971-2018:Estimating a Reaction Function Using the Best Proxy』:先行研究解説 No.12💝2023/10/31

Introduction:卒業論文は早めに仕上げたい💛

私もいよいよ卒業論文の執筆に

取りかかる時期がやって参りました👍

何事もアウトプット前提のインプットが

大事であると、noteで毎日発信してきました

これは、どのような内容で

あっても当てはまります👍

論文を一概に読んでも

記憶に残っていなかったり

大切な観点を忘れてしまっていたりしたら

卒業論文の進捗は滞ってしまうと思います

だからこそ、この「note」をフル活用して

卒業論文を1%でも

完成に向けて進めていきたいと思います

私の卒論執筆への軌跡を

どうぞご愛読ください📖

今回の参考文献🔥

今回、読み進めていく論文は

こちらのURLになります👍

『Japanese Foreign Exchange Interventions, 1971-2018: Estimating a Reaction Function Using the Best Proxy』

Takatoshi Ito(a), Tomoyoshi Yabu(b)

(a) School of International and Public Affairs, Columbia University, and GRIPS, Tokyo

(b) Department of Business and Commerce, Keio University

Japanese Foreign Exchange Interventions, 1971-2018: Estimating a Reaction Function Using the Best Proxy

December 12, 2019

Takatoshi Ito(a), Tomoyoshi Yabu(b)

(a) School of International and Public Affairs, Columbia University, and GRIPS, Tokyo

(b) Department of Business and Commerce, Keio University

前回のお復習い📝

5. Reaction Function

In this section, we estimate the monetary authorities’ reaction function using the data from August 1971 to March 2018.

Most papers analyzing interventions before March 1991 have used “Change in Reserve” or “Treasury Funds and Others/Foreign Exchange” as a proxy for interventions.

What differentiates this paper from these previous papers is the use of the proxy Ito and Yabu (2017) identified and also the adoption of an up-to-date reaction function proposed by Ito and Yabu (2007).

このセクション5では、1971年8月から2018年3月までのデータを使用して金融当局の反応関数(the monetary authorities’ reaction function)を推定します

1991年3月以前の介入を分析するほとんどの論文は、「準備金の変動」または「財務資金およびその他/外国為替」を代理変数(Proxy)として使用しています

この論文がこれらの以前の論文と異なるポイントは、Ito and Yabu (2017) が特定した代用関数を使用していることと、Ito and Yabu (2007) によって提案された最新の反応関数を採用していることになります

5.1. Ordered Probit Model

Almekinders and Eijffinger (1996) were the first to derive a reaction function from a loss function of monetary authorities.

Ito and Yabu (2007) extended their model by allowing for a more realistic formulation of the target exchange rate and a cost function of interventions to derive a reaction function as an ordered probit model.

The ordered probit model of Ito and Yabu (2007) is the following:

AlmekindersとEijffinger(1996)は、金融当局の損失関数から反応関数を導出した最初の研究者になります📝

Ito and Yabu (2007)は、目標為替レートと介入のコスト関数をより現実的に定式化して、順序付けされたプロビットモデルとして反応関数を導出できるようにすることでモデルを拡張しました

Ito and Yabu (2007)の順序付けプロビットモデルは次のとおりです

$$

\\Ordered Probit Model \\ \\IInt_t = \begin{cases}

+1 &\text{if } \mu_2 < y_t^* \\

0 &\text{if } \mu_1 < y_t^* < \mu_2 \\ -1&\text{if } y_t^* < \mu_1 \cdots(2)

\end{cases} \\ \\ \\where y_t^*=X_t\beta +\epsilon_t \\with \epsilon_t \backsim i.i.d N(0,\sigma^2) and\\ \\X_t\beta=\beta_1(s_{t-1}-s_{t-2})+\beta_2(s_{t-1}-s_{t-1}^{MA})+\beta_3 IInt_{t-1}

$$

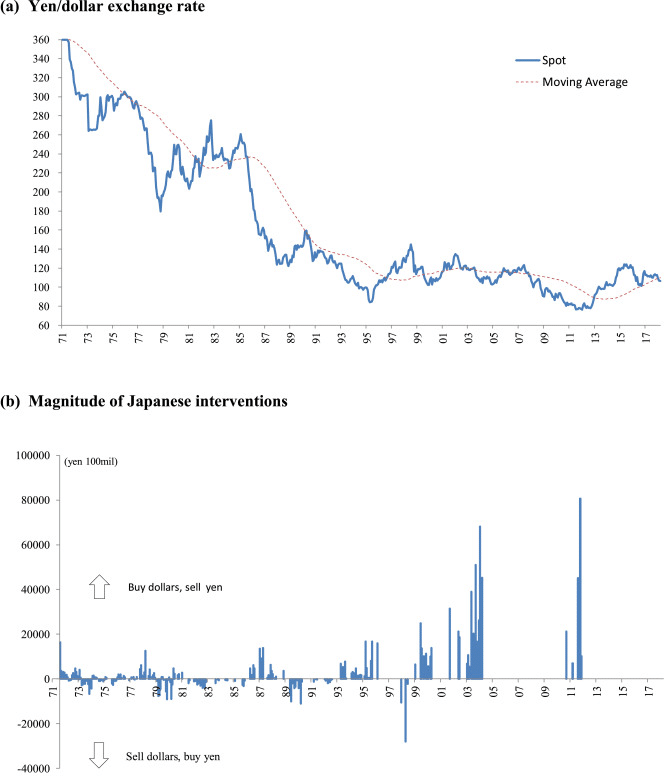

Here IInt_t takes a value of + 1 if there is dollar-purchasing intervention, if there is dollar-selling intervention, and 0 if there is no intervention.

The log of the monthly yen/dollar rate is denoted by st and the log of the moving average yen/dollar rate over the past five years by s_t^MA.

The lag of IInt_t is included to explain a positive autocorrelation of interventions, i.e., when there is intervention one month, it is likely that intervention will take place in the following month.

The latent variable yt* represents the optimal amount of intervention and intervention does not take place as long as yt* is inside a “neutral band” of no intervention, i.e., [μ1, μ2].

ここで、プロビットモデルにおける被説明変数であるIInt_t は次の値を取るように設定されています

ドル買い(円売り)介入があれば、+1

介入が実施されなければ、0

ドル売り(円買い)介入があれば、-1

なお、月々の円/ドルレートの対数は、stで表されています

また s_t^MA な過去5年間の円/ドル移動平均(Moving Average)レートの対数値になります📝

そして IInt_t のラグは、介入の正の自己相関(positive autocorrelation of interventions)を説明するために含まれています

つまり、介入がある月に実施された場合、その介入は翌月に行われる可能性が高いという解釈になります

潜在変数yt*は最適な介入量を表し、この値が「ニュートラルバンド:neutral band」つまり [μ1, μ2]内にある場合、介入が実施されることは無くなります

Regarding the parameters of the model, the parameter β1 takes a negative value (β1 < 0) when there is lean-against-the-wind intervention and β2 takes a negative value (β2 < 0) when policy makers have a long-run target in mind.

On the other hand, the parameter β3 takes a positive value (β3 > 0) when there is intervention one month and intervention is likely to take place in the following month.

Here, μ1 represents the cost of dollar-selling intervention while μ2 is the cost of dollar-buying intervention. The cost of interventions is introduced to explain the fact that interventions do not take place every month.

We estimate this model using the maximum likelihood method but identify only the normalized parameters β*≡ βi/ σ and µ*≡

µi/σ, not the parameters βi and μi themselves.

プロビットモデルのパラメータに関しては、風に逆らう介入(lean-against-the-wind intervention)がある場合、パラメータ β1は負の値 (β1 < 0) をとり、政策立案者が長期目標(long-run target)を念頭に置いて持っている場合、パラメータ β2は負の値 (β2 < 0) をとります

一方、介入がある月に実施され、次の月にも介入が行われる可能性が高い場合、パラメータ β3 は正の値(β3 > 0)になります📝

ここで、μ1はドル売り介入のコスト、μ2はドル買い介入のコストを表していることに留意します

なお、この介入のコスト(μ1,μ2)は、介入が毎月行われるわけではないという事実を説明するために導入されています

最尤法を使用してこのモデルを推定しますが、パラメータ βi および μi 自体ではなく、正規化されたパラメータ β≡ βi/ σ および µ≡ µi/σ のみを識別することになる点には注意が必要ですね📝

本日の解説は、ここまでとします

このような歴史や先行研究をしっかり理解した上で、卒業論文執筆に取り組んでいきたいです

読み終えた先行研究📚

『日本の為替介入の分析』 伊藤隆敏・著

経済研究 Vol.54 No.2 Apr. 2003

『Effects of the Bank of Japan’s intervention on yen/dollar exchange rate volatility』21 November 2004

Toshiaki Watanabe (a), Kimie Harada (b)

『The Effects of Japanese Foreign Exchange Intervention: GARCH Estimation and Change Point Detection』

Eric Hillebrand Gunther Schnabl Discussion

Paper No.6 October 2003

私の研究テーマについて🔖

私は「為替介入の実証分析」をテーマに

卒業論文を執筆しようと考えています📝

日本経済を考えたときに、為替レートによって

貿易取引や経常収支が変化したり

株や証券、債権といった金融資産の収益率が

変化したりと日本経済と為替レートとは

切っても切れない縁があるのです💝

(円💴だけに・・・)

経済ショックによって

為替レートが変化すると

その影響は私たちの生活に大きく影響します

だからこそ、為替レートの安定性を

担保するような為替介入はマクロ経済政策に

おいても非常に重要な意義を持っていると

推測しています

決して学部生が楽して執筆できる

簡単なテーマを選択しているわけでは無いと信じています

ただ、この卒業論文をやり切ることが

私の学生生活の集大成となることは事実なので

最後までコツコツと取り組んで参ります🔥

本日の解説は、以上とします📝

今後も経済学理論集ならびに

社会課題に対する経済学的視点による説明など

有意義な内容を発信できるように

努めてまいりますので

今後とも宜しくお願いします🥺

マガジンのご紹介🔔

こちらのマガジンにて

卒業論文執筆への軌跡

エッセンシャル経済学理論集、ならびに

【国際経済学🌏】の基礎理論をまとめています

今後、さらにコンテンツを拡充できるように努めて参りますので何卒よろしくお願い申し上げます📚

最後までご愛読いただき誠に有難うございました!

あくまで、私の見解や思ったことを

まとめさせていただいてますが

その点に関しまして、ご了承ください🙏

この投稿をみてくださった方が

ほんの小さな事でも学びがあった!

考え方の引き出しが増えた!

読書から学べることが多い!

などなど、プラスの収穫があったのであれば

大変嬉しく思いますし、投稿作成の冥利に尽きます!!

お気軽にコメント、いいね「スキ」💖

そして、お差し支えなければ

フォロー&シェアをお願いしたいです👍

今後とも何卒よろしくお願いいたします!

この記事が気に入ったらサポートをしてみませんか?