【記述統計とデータの特徴📊】Official Japanese Intervention in the JPY/USD Exchange Rate Market: Is It Effective and Through Which Channel Does It Work?🌟BoJ Report No.4📚

卒業論文を書き終えて💛

先日、大学を無事卒業した私ですが

卒業論文で「優秀論文賞」を受賞

することができました🏆

何事もアウトプット前提の

インプットが大事であると

noteで毎日発信してきました📢

これは、どのような内容で

あっても当てはまりますね👍

先行研究を一概に読んでも

記憶に残っていなかったり大切な観点を

忘れてしまっていたりしたら

卒業論文の進捗は滞っていたでしょう💦

なお、この投稿では収益化をすることはなく

先行研究などのコンテンツを正しく引用し

適切な発信ができるように努めます📝

私の卒論執筆への軌跡を

どうぞ最後までご愛読ください📖

今回の参考文献🔥

今回、読み進めていく論文は

こちらになります📚

Official Japanese Intervention in the JPY/USD Exchange Rate Market: Is It Effective and Through Which Channel Does It Work?

Rasmus Fatum*

IMES Discussion Paper Series

2009-E-12 March 2009

前回のお復習い✨

2. Data

The official Japanese intervention data consists of daily volumes of intervention operations in the JPY/USD foreign exchange market.

During the period under study, January 1999 to March 2004, all official interventions in the JPY/USD market are sales of JPY against purchases of USD.12

12:The U.S. government did not intervene in the JPY/USD exchange rate market during this period.

日本の公式介入データは、JPY/USD外国為替市場における日次の介入操作の額(daily volumes of intervention operations)で構成されます。

1999年1月から2004年3月までの調査対象期間中、JPY/USD市場へのすべての公式介入は、USDの購入に対するJPYの売りでした(注12)。

※円高水準を是正する介入であったということです。

12: この期間、米国政府は、JPY/USD為替市場に介入しませんでした。

※日本の通貨当局による単独介入です。

Table 1 shows intervention data summary statistics.

The table shows that Japan intervenes in the JPY/USD exchange rate market on a total of 159 days over the full sample period.

On most intervention days the magnitude of intervention is substantial, with purchases of over USD 1,000 million on 113 days and only 20 days with purchases of less than USD 250 million.

The table shows that only 30 of the intervention days occur between January 1999 and December 2002, 82 intervention days occur during 2003, while 47 intervention days occur during the first quarter of 2004.13

13:Fatum and Hutchison (2006b) show that the described variation in intervention frequencies over the January 1999 to March 2004 time period is consistent with the existence of three different intervention reaction function regimes.

表1は、介入データの要約統計を示しています。

この表は、日本がサンプル期間全体で合計159日間、円/米ドル為替市場に介入していることを示しています。

ほとんどの介入日では介入の規模が大きく(the magnitude of intervention is substantial)、113日間で10億米ドルを超える購入が行われましたが、購入金額が2億5,000万ドル未満の場合はわずか20日間でした。

この表は、1999年1月から2002年12月までの間に介入日はわずか30日であり、2003 年には介入日が82日あったのに対し、2004年の第1四半期には介入日が47日であることを示しています(注13)

※各財務官によって運営方針が異なっていますね👀

13: Fatum and Hutchison (2006b)は、記載されている変動が1999 年 1 月から 2004 年 3 月までの期間にわたる介入頻度は、3つの異なる介入反応関数レジームの存在と一致しています。

In order to compare the exchange rate effect of interventions that the market seem aware of to interventions that the market seem unaware of and, in turn, attempt to shed light on through which transmission channel intervention works, rumors of intervention are taken into account.

The analysis distinguishes between a rumor of intervention and a firm report of intervention, and only incorporates the former for the following reason.

A rumor of intervention occurs on the same day that the market thinks an intervention takes place, while a firm report of intervention typically occurs the day after the intervention has taken place.14

Therefore, whether or not an intervention is reported is generally a matter of “after-the-fact” information that can not play a role in the contemporaneous exchange rate response to intervention.

By contrast, whether or not an intervention coincides with a rumor seems a better indicator of whether the market is aware of the intervention operation the same day it is carried out.

Moreover, whether the market is aware of the intervention operation may affect the same-day market reaction to intervention as well as trigger a same-day market reaction to the rumor itself (whether or not intervention actually occurs.) 15

市場が認識していると思われる介入の為替レートへの影響と、市場が認識していないように見える介入の為替レートへの影響を比較し、その結果、どの伝達経路を通じて介入が機能するかを明らかにするために、介入の噂(rumors of intervention)が考慮されます。

実証分析では介入の噂と介入の確定報告が区別され、次の理由により前者のみが組み込まれます。

介入の噂は市場が介入が行われたと考えるのと同じ日に発生しますが、介入の確定報告は通常発生します(注14)。

したがって、介入が報告されるかどうかは一般に「事後」情報の問題(“after-the-fact” information)であり、介入に対する同時期の為替レートの反応に役割を果たすことはできません。

介入が噂と一致するかどうか(whether or not an intervention coincides with a rumor)は、市場が介入操作が実行された日にそのことを認識しているかどうかを示すより良い指標であると思われます。

さらに、市場が介入操作を認識しているかどうかは、その日の市場の反応に影響を与える可能性があります。

介入を行うだけでなく、その噂自体に対する同日の市場の反応を引き起こすこともある(実際に介入が行われるかどうかは別として)ことを抑えておきましょう(注15)。

14: For example, a firm report of the January 12, 1999 official Japanese intervention operation is reported on the newswire on January 13, 1999.

15: For completeness, Factiva was also gleaned for firm reports of intervention.

For the full sample, a total of 31 firm reports of intervention were found. To compare, Chang (2006) finds 27 firm reports of intervention in the Wall Street Journal over the January 2000 to March 2003 time period.

While most Bank of Japan interventions are unreported, no false firm reports of intervention were found.

By contrast, more than half of the interventions under study coincide with a rumor and, furthermore, several “false” rumors of intervention (i.e. a rumor of intervention when no intervention takes place) were found.

This further illustrates the importance of distinguishing between reports of intervention and rumors of intervention.

14:例えば、1999年1月12 日の日本の公的な介入作戦に関する確固たる報告書は、1999年1月13日のニュースワイヤーで報じられています。

15: 完全を期すために、ファクティバ(Factiva)社の介入に関する確固たる報告書も収集されています。

完全なサンプルでは、合計31件の介入に関する企業報告が見つかりました。

比較するために、Chang(2006)は、2000年1月から2003年3月までの期間にウォール ストリート ジャーナル(the Wall Street Journal)に掲載された27件の確実な介入報告を発見しました。

日銀介入のほとんどは報告されていませんが、介入に関する虚偽の企業報告は見つかってもいません。

対照的に、研究中の介入の半分以上は噂と一致しており、さらに介入に関する「誤った」噂(つまり、介入が行われていないのに介入があるという噂)がいくつか見つかりました。

これは、介入の報告と介入の噂を区別することの重要性(importance of distinguishing between reports of intervention and rumors of intervention)をさらに示しています。

The Factiva search engine and a comprehensive combination of various search words (e.g. Bank of Japan, intervention etc.) are used to find the days with a rumor of intervention.

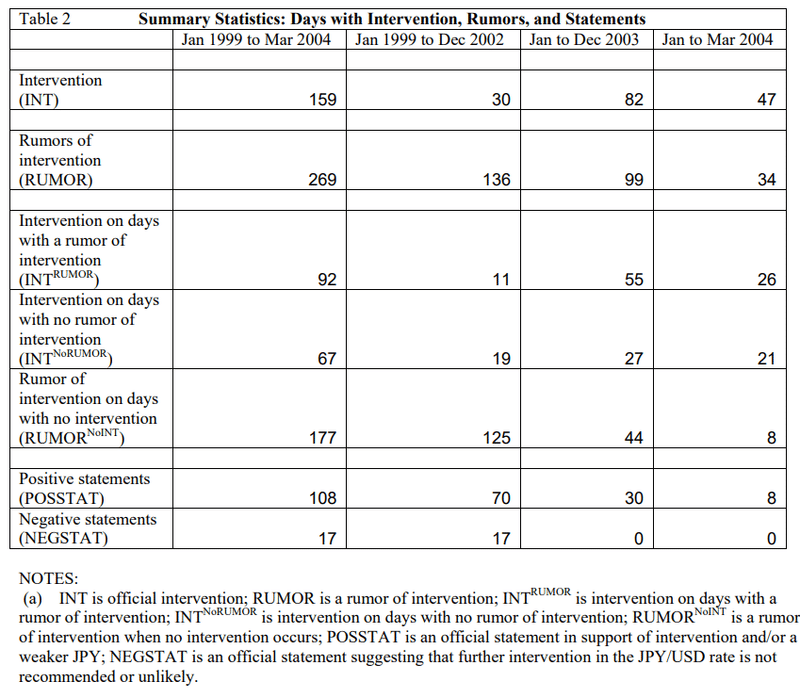

The second row of Table 2 shows that a total of 269 days across the full sample are associated with a rumor of intervention.

Row three of Table 2 reports that 92 of the rumor days are also intervention days, i.e. 92 of the 269 rumors are “true”.

Row four shows that, accordingly, the remaining 67 of the 159 intervention days in the full sample do not coincide with a rumor of intervention. For the full sample, as many as 177 rumor days are, in fact, “false”.

The numbers of days associated with false rumors are reported in row five. 16

16: It is not surprising to find a large number of false rumors of intervention. Chang (2006) reports a total of 282 JiJi News (local Japanese newswire) and Wall Street Journal reports of rumors and speculation of Japanese intervention over the January 2000 to March 2003 time period.

Moreover, other studies question the accuracy of newswire reports of intervention (see Fischer 2006 and Osterberg and Wetmore Humes 1993).

ファクティバ検索エンジンとさまざまな検索ワード(例:日銀、介入など)を総合的に組み合わせて、介入の噂がある日を検索します。

表2の2行目は、サンプル全体の合計269日が介入の噂と関連していることを示しています。

表2の3行目は、噂日のうち92日が介入日でもあること、つまり269件の噂のうち92日が「真実」であることを報告しています。

したがって、4行目は、サンプル全体の介入日159日のうち残りの 67 日が介入の噂と一致しないことを示しています。

完全なサンプルの場合、実際には 177 日もの噂が「虚偽」です。

虚偽の噂に関連する日数が5行目に報告されます(注16)。

16:介入に関するデマが大量に見つかっても不思議ではありません。

Chang (2006) は合計282件のJiJi(日本のローカルニュースワイヤー)の日本の介入に関する噂と憶測に関するニュースとウォール・ストリート・ジャーナルの報道は2000 年1月から2003年3月までの期間にわたっていました。

さらに、他の研究ではニュースワイヤーの正確性に疑問を呈しています。

また、介入に関する報告書 (Fischer 2006 および Osterberg および Wetmore Humes 1993 を参照)もあります。

Some studies suggest that official statements regarding threats of intervention or regarding the desired direction of future exchange rate movements (sometimes referred to as “oral interventions”) influence exchange rate.

In order to take into account this possibility, the analysis uses the Factiva search engine to find, respectively, newswire reports of official statements in support of intervention and/or a weaker JPY (“positive statements”), and newswire reports of official statements suggesting that further intervention in the JPY/USD rate is not recommended or unlikely (“negative statements”).

Rows six and seven of Table 2, respectively, report a total of 108 positive and 17 negative statements for the full sample period.

一部の研究は、介入の脅威や将来の為替レートの望ましい方向性に関する公式声明(「口頭介入(“oral interventions”)」と呼ばれることもあります)が為替レートに影響を与えることを示唆しています。

この可能性を考慮するために、分析ではファクティバ検索エンジンを使用して、介入および/または円安を支持する公式声明のニュースワイヤー報道(「肯定的な声明“positive statements”」)と、介入および/または円安を示唆する公式声明のニュースワイヤー報道をそれぞれ検索しました。

JPY/USD レートへのさらなる介入は推奨されないか、その可能性は低いと述べています (「否定的な記述“negative statements”」)。

なお表2の6行目と7行目は、サンプル期間全体で合計108件の肯定的な発言と17件の否定的な発言をそれぞれ報告しています。

本日の解説はここまでとします💖

この先行研究は非常に有意義であり

大変勉強になりました✨

読み終えた先行研究📚

『日本の為替介入の分析』

伊藤隆敏・著

経済研究 Vol.54 No.2 Apr. 2003

『Effects of the Bank of Japan’s intervention on yen/dollar exchange rate volatility』21 November 2004

Toshiaki Watanabe (a), Kimie Harada(b)

『The Effects of Japanese Foreign Exchange Intervention: GARCH Estimation and Change Point Detection』

Eric Hillebrand Gunther Schnabl Discussion

Paper No.6 October 2003

Author/Editor:Jaromir Benes ; Andrew Berg ; Rafael A Portillo ; David Vávra

Publication Date: January 14, 2013

私の研究テーマについて🔖

私は「為替介入の実証分析」をテーマに

卒業論文を執筆しようと考えています📝

日本経済を考えたときに、為替レートによって

貿易取引や経常収支が変化したり

株や証券、債権といった金融資産の収益率が

変化したりと日本経済と為替レートとは

切っても切れない縁があるのです💝

(円💴だけに・・・)

経済ショックによって為替レートが

変化するとその影響は

私たちの生活に大きく影響します。

だからこそ、為替レートの安定性を

担保するような為替介入はマクロ経済政策に

おいても非常に重要な意義を持っていると

推測しています。

卒業論文をやり切ることが私の学生生活の

集大成となることは事実ですので

最後までコツコツと取り組み、良い結果を

得ることができたのは嬉しかったです🔥

本日の解説は、以上とします📝

今後も経済学理論集ならびに社会課題に

対する経済学的視点による説明など

有意義な内容を発信できるように

努めてまいりますので

今後とも宜しくお願いします🥺

マガジンのご紹介🔔

最後までご愛読いただき誠に有難うございました!

あくまで、私の見解や思ったことを

まとめさせていただいてますが

その点に関しまして、ご了承ください🙏

この投稿をみてくださった方が

ほんの小さな事でも学びがあった!

考え方の引き出しが増えた!

読書から学べることが多い!

などなど、プラスの収穫があったのであれば

大変嬉しく思いますし、投稿作成の冥利に尽きます!!

お気軽にコメント、いいね「スキ」💖

そして、お差し支えなければ

フォロー&シェアをお願いしたいです👍

今後とも何卒よろしくお願いいたします!

この記事が気に入ったらサポートをしてみませんか?