[決算速報][3M Company] 2024年第1四半期(2024年1月~3月)

オリジナルデータ

URL : https://investors.3m.com/

3M Company の2024年第1四半期の決算が2024年4月30日(火)、米国株式市場Open前に発表されました。

Financial Highlights

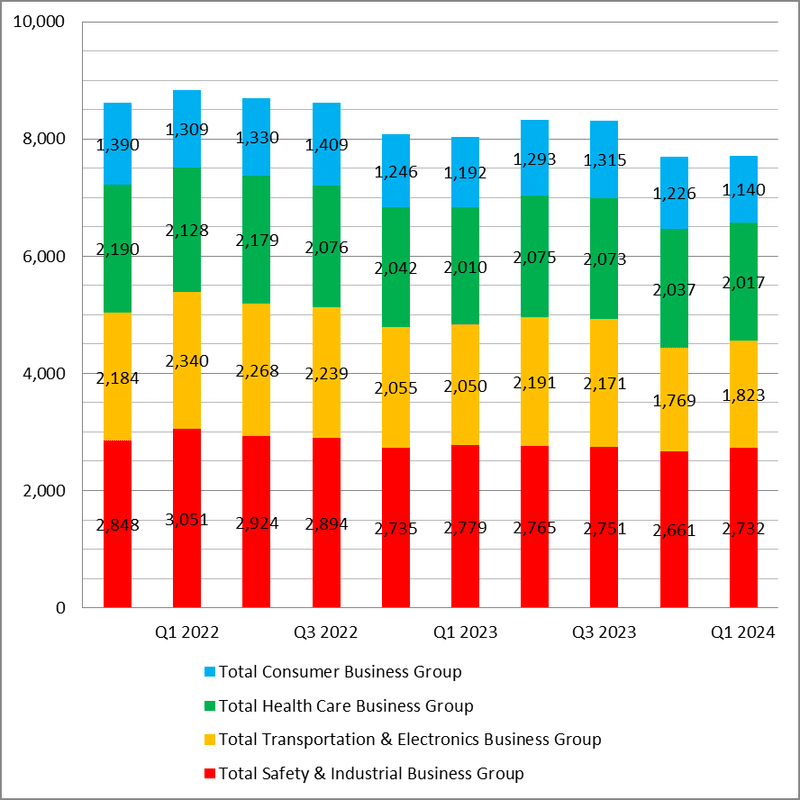

部門別売上高の推移配下のグラフのとおりです。いちばん右が2024年第1四半期の結果です。前期からほぼ横ばい。第2四半期からはヘルスケア部門の売上(緑の棒)がごっそり抜けます。

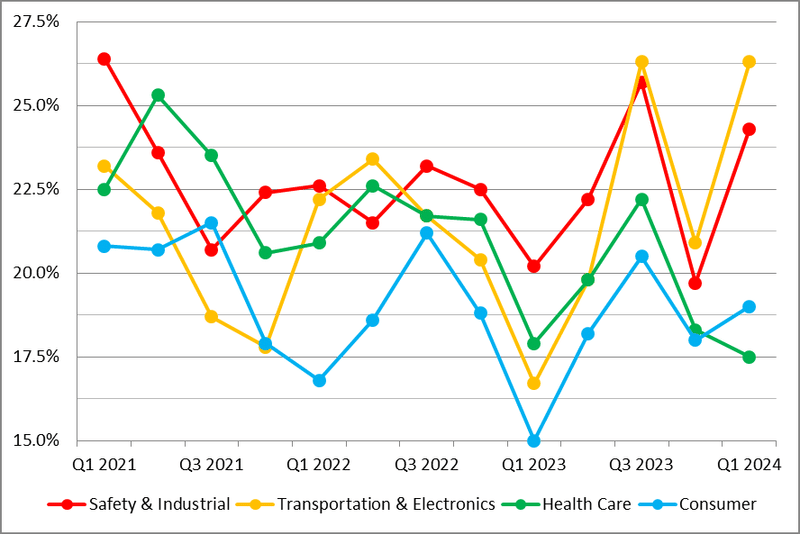

部門別の調整後営業利益率の推移配下のグラフのとおりです。前期は産業部門(赤、黄)で少しガクっと下がりましたが、今期はV字回復しています。

Press release

Press release に自信満々なCEOのコメントが載っています。

We delivered results that were better than our expectations as we returned to organic growth and achieved double digit adjusted earnings growth. We improved performance in our businesses through strong operational execution, completed the spin-off of Solventum, and finalized two major legal settlements.

The progress we have made in executing our strategic priorities, positions the company for long-term shareholder value creation as Bill Brown assumes the role of 3M CEO.

曰く、

期待以上の結果だ。売上は成長基調に戻ったし、調整後利益は2桁成長を達成した。事業の経営数字は改善し、Solventum(ヘルスケア部門)のスピンオフを完了し、大きな訴訟案件2つを終わらせた。

戦略的優先事項を進めた。長期的な株主価値創造につながるだろう。

Presentation

各事業の状況など詳細はPresentationを確認していきます。

Q1 2024 actuals and full-year earnings outlook approach

3月末にヘルスケア部門のスピンオフが完了して最初の決算発表なので、それを踏まえた2024年通期見通しが公表されました。

ヘルスケア部門は非継続事業という扱いになります。

ヘルスケア部門が Solventum Corporation としてスピンオフ後も3M Company はその株式の19.9%を保有しています。この株式持分から発生する利益は Non-GAAPの利益に反映されます。

Strong execution, significant progress on priorities

Driving performance through the 3M model

• Adjusted revenue of $7.7B, improved organic growth

• Delivered adjusted OI margin of 21.9%, up 400 basis points YoY

• Adjusted EPS of $2.39, up double-digits YoY

• $0.8B of adjusted free cash flow; remain focused on working capital improvement

Spinning off Health Care

• Successfully completed the spin of Solventum on April 1st

• 3M shareholders received 80.1% of Solventum shares

• 3M received $7.7B in cash and retained 19.9% of shares

• Creates two world-class publicly held companies

Reducing risk and uncertainty

• Public Water Suppliers (PWS) settlement received final court

approval

• Well over 99% of eligible Combat Arms Earplugs claimants have chosen to participate in the settlement

• On track to exit all PFAS manufacturing by year-end 2025

業績について

売上高(調整後)は77億ドル、成長基調に戻った。

調整後営業利益率は21.9%、前年同期比4%アップ。

調整後1株利益は$2.39、前年同期比2桁の伸び。

フリーキャッシュフロー(調整後)は8億ドル。

ヘルスケア部門のスピンオフについて

4/1 にスピンオフが完了した。

3M Company の株主には、Solventumの株式の80.1%を分配した。

3M Company は77億ドルの現金と19.9%のSolventum株を受け取った。

上場会社が新たに誕生した(ヘルスケア部門は Solventum Corporationとしてニューヨーク証券取引所に上場した)。

リスクの低減

水道事業者による訴訟案件は、裁判所の最終承認を得た。

耳栓訴訟案件では、99%以上の原告と和解した。

PFAS(結城フッ素化合物)の生産からは2025年末までに完全撤退する。

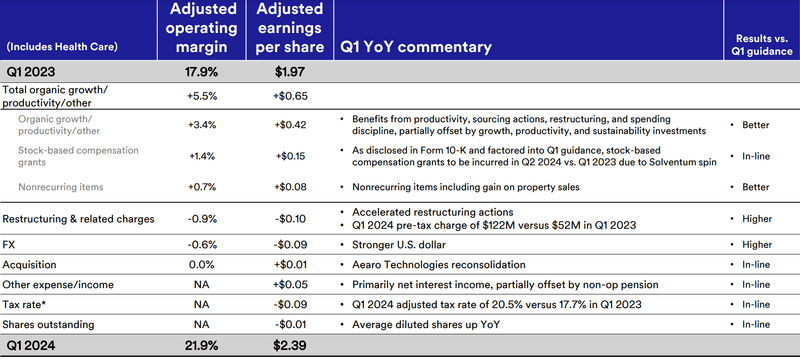

Q1 2024 operating margin and EPS

調整後営業利益率は、前年同期の17.9%から21.9%に改善しています。リストラ費用、為替の悪影響(ドル高なのでUSA以外での売上、利益にマイナス)によるマイナス影響(マイナス1.5%)を、それを大きく上回るOrganic growth と生産性の改善(プラス5.5%)で吹き飛ばしています。

Organic growth は Underlying growth と同義です。基調的な売上成長率。事業売却や事業買収といった特殊要因の影響を除いた売上の成長率と考えてよいでしょう。以降、頻繁に出てくるので憶えておいてください。

Safety & Insudtrial

Organic growth はマイナス1.4%、調整後営業利益率は24.3%

Organic growth performance:

– Mid-teens increase in roofing granules; low-single digit increase in industrial adhesives and tapes

– Low-single digit decline in electrical markets, abrasives, automotive aftermarket, and personal safety; high-single digit decline in industrial specialties

– Disposable respirator YoY headwind of ~$25M; reduced segment organic growth by 80 bps

• Adjusted operating margin up 410 bps YoY; up 460 bps sequentially

– YoY increase driven by:

▪ Benefits from productivity actions, restructuring, strong spending discipline, and stock-based compensation grants to be incurred in Q2 2024 vs. Q1 2023

▪ Partially offset by decline in organic sales volume and restructuring costs

売上について

屋根の補修材の売上が15%前後伸長した。

産業用の接着剤やテープの売上が1~4%伸長した。

電機、研磨剤、自動車アフターマーケット、個人向けの安全器具の売上は1~4%減少した。

産業用特殊薬品の売上は6~9%減少した。

マスクの売上は前年比2,500万ドル減少し、セグメント売上を0.8%押し下げた。

調整後営業利益率は前年比4.1%、前期比4.6%改善した。

生産性の改善、リストラ、財務規律の徹底、株式報酬費用の前年比減少が寄与し、販売数量の減少というマイナス要因を補った。

Transportation & Electronics

Organic growth(調整後)はプラス6.7%、調整後営業利益率は26.3%

Adjusted organic growth performance

– Mid-teens increase in electronics; mid-single digit increase in automotive and aerospace; low-single digit increase in commercial branding and transportation; advanced materials flat

• Strong momentum in automotive electrification

• Share gains with spec-in wins and new product introductions in automotive and consumer electronics; drove strong volume growth to support customer production ramp and product launches

• Inventory normalization in electronics and automotive channels

• Adjusted operating margin up 960 bps YoY; up 540 bps sequentially

– YoY increase driven by:

▪ Benefits from strong leverage on organic sales volumes growth, productivity actions, restructuring, strong spending discipline, and stockbased compensation grants to be incurred in Q2 2024 vs. Q1 2023

▪ Partially offset by restructuring costs

売上について

電気関連で売上が15%前後伸長した。

自動車、宇宙関連で5%前後売上が伸長した。

ブランディング、輸送関連で1~4%売上が伸長した。

特殊材料の売上はほぼ変わらず。

電気自動車関連の需要が強い。

自動車、消費者向け電気製品でシェア拡大。販売数量増加。

電気、自動車分野で在庫の適正化が進んでいる。

調整後営業利益率は前年同期比9.6%、前期比5.4%改善した。

販売数量増加、生産性の改善、リストラ、財務規律の徹底、株式報酬費用の前年比減少が寄与し、リストラ費用の発生による悪影響を補った。

Consumer

Organic growth はマイナス1.9%、営業利益率は19.0%

• Organic growth performance

– Low-single digit decline in home improvement, and consumer safety and well-being

– Mid-single digit decline in home and auto care

– High-single digit decline in packaging and expression

• Continued softness in consumer discretionary spend; and product portfolio and geographic prioritization headwind

• Investing in the business including supporting successful new product launches

• Operating margin up 400 bps YoY; up 100 bps sequentially

– YoY increase driven by:

▪ Benefits from productivity actions, restructuring, portfolio initiatives, strong spending discipline, and stock-based compensation grants to be incurred in Q2 2024 vs. Q1 2023

▪ Partially offset by decline in organic sales volume and restructuring costs

売上について

Home Improvement、Consumer Safety、Well-being の売上が1~4%程度減少。

Home and Auto Care の売上が5%前後減少。

Packaging and Expression の売上が6~9%減少。

生活必需品以外の消費が弱い。

新製品の発売などに向け投資を実行。

営業利益率は前年同期比4%、前期比1%改善。

生産性の改善、リストラ、財務規律の徹底、株式報酬費用の前年比減少が寄与し、販売数量の減少というマイナス要因を補った。

Initiating 2024 full-year earnings guidance on a continuing operations basis

2024年通期見通しは以下のとおりです。

Organic sales growth(調整後)は 0%~+2%

2023年のマイナス4.4%から改善

調整後営業利益率は20.7%~21.45%

2023年比で2%~2.75%改善

継続事業の調整後1株利益は$6.80~$7.30

この利益にはスピンオフしたヘルスケア部門の利益は含まれません(スピンオフ前の1~3月分も)。

年前半よりも後半の方が若干売上、利益とも多くなると見込んでいます。

Resetting our dividend post Solventum spin

ヘルスケア部門のスピンオフにより、3M Company 自体の売上と利益は当然ながら減少します。配当がどうなるか、は株主にとって大きな関心事項ですが、これに関して言及があります。

• Following the spin of Solventum, 3M’s dividend payout ratio is expected to be approximately 40% of adjusted free cash flow with potential to increase over time

• Second quarter dividend expected to be declared in May 2024, subject to board approval

• Share repurchases – stepped back into the market

Solventumのスピンオフに伴い、3M Company が支払う配当は、調整後フリーキャッシュフローの約40%と見込まれる(ただしフリーキャッシュフローは時間とともに成長すると見込んでいる)。

第2四半期の配当は、5月に取締役会で決定する。

自己株式の買い付けは縮小するか停止する。

この書き方からして、おそらく24年2Qの配当は減配になるだろうと思います。フリーキャッシュフローの40%を配当すると言っていますし、23年の配当額もフリーキャッシュフローのだいたい40%でした。ヘルスケア事業からのキャッシュインがなくなるので、まちがいなくフリーキャッシュフローは減るはずです。自己株式の買い付けも step back(後退する)と言っているので、キャッシュインが減った分キャッシュアウトも抑制するのでしょう。

健全な経営ですばらしいですが、60年以上続いた 3M Company の連続増配記録は、ついにストップしてしまうかもしれません。😥

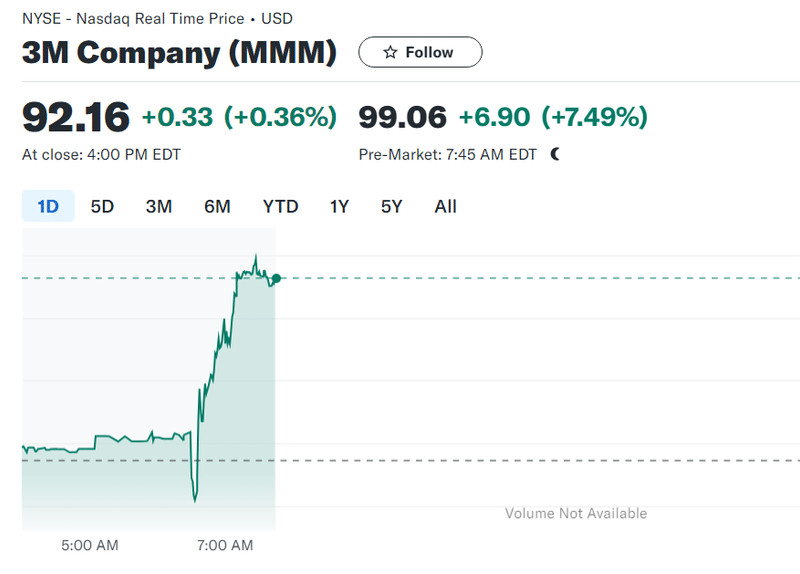

Pre-Marketの反応

Pre-Marketの反応は好調です。

前日終値に比べて7%以上値上がりしています。

関連記事

この記事が気に入ったらサポートをしてみませんか?