【協調介入の歴史と極めて有効な影響🌏】『Japanese Foreign Exchange Interventions, 1971-2018:Estimating a Reaction Function Using the Best Proxy』:先行研究解説 No.15💝2023/11/04

Introduction:卒業論文は早めに仕上げたい💛

私もいよいよ卒業論文の執筆に

取りかかる時期がやって参りました👍

何事もアウトプット前提のインプットが

大事であると、noteで毎日発信してきました

これは、どのような内容で

あっても当てはまります👍

論文を一概に読んでも

記憶に残っていなかったり

大切な観点を忘れてしまっていたりしたら

卒業論文の進捗は滞ってしまうと思います

だからこそ、この「note」をフル活用して

卒業論文を1%でも

完成に向けて進めていきたいと思います

私の卒論執筆への軌跡を

どうぞご愛読ください📖

今回の参考文献🔥

今回、読み進めていく論文は

こちらのURLになります👍

『Japanese Foreign Exchange Interventions, 1971-2018: Estimating a Reaction Function Using the Best Proxy』

Takatoshi Ito(a), Tomoyoshi Yabu(b)

(a) School of International and Public Affairs, Columbia University, and GRIPS, Tokyo

(b) Department of Business and Commerce, Keio University

Japanese Foreign Exchange Interventions, 1971-2018: Estimating a Reaction Function Using the Best Proxy

December 12, 2019

Takatoshi Ito(a), Tomoyoshi Yabu(b)

(a) School of International and Public Affairs, Columbia University, and GRIPS, Tokyo

(b) Department of Business and Commerce, Keio University

前回のお復習い📝

6. International Coordination or non-Coordination

6.1. Policy coordination on exchange rates

The Group of Seven (G7) monetary authorities were engaged in interventions very frequently during the 1970s and 1980s. However, the frequency of interventions declined during the 1990s.

Frequent interventions by the US, Germany and the UK ceased by 1995.

The frequency of Japanese intervention also declined after 1995, apart from 14 months of frequent interventions from January 2003 to March 2004.

主要7カ国(G7)金融当局は、1970年代から1980年代にかけて非常に頻繁に介入を実施していました

しかし、介入の頻度は1990 年代になると減少しています

米国、ドイツ、英国による頻繁な介入は1995年までに終了したと考察できます

そして、日本の介入頻度も、2003年1月から2004年3月までの14 か月にわたる頻繁な介入を除けば、1995年以降減少したと言えるでしょう

During the period of frequent interventions, there were many cases where two or three of the G3—the US, Japan and Germany—intervened in the same direction simultaneously.

There were also cases of US-Japan joint interventions; US-German joint interventions and even three-way interventions.

When engaging in joint interventions, they must have shared the same views in terms of the level and movement of the exchange rate, such as the idea that since the US dollar is overvalued, the US should buy German marks and Japanese yen, while Germany and Japan should sell US dollars.

When two or three authorities intervene in the same direction in the same month, we refer to them as “coordinated interventions” throughout the rest of the paper.

介入が頻繁に行われた時期には、G3のうち米国、日本、ドイツの2~3か国が同時に同じ方向に介入するケースが多かったようです

時には、米独共同介入、さらには三者介入も存在しています

また、共同介入を行う際には、為替レートの水準や動向について同じ認識を共有していたはずです

ここで、ドルが過大評価されている状況を踏まえたら、米国はドイツマルクと日本円を購入し、ドイツと日本は米ドルを売るべきであると考えられます

2つまたは3つの通貨当局が、同じ月に同じ方向に介入する場合、本稿の残りの部分ではそれらを「協調介入(“coordinated interventions”)」と呼びます

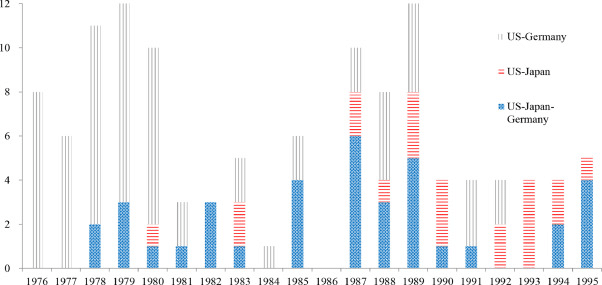

Fig. 6 shows that the number of months per year during which the authorities coordinated their interventions from 1976 to 1995.

For example, in 1979, US-German joint interventions were conducted during nine months and US-German-Japanese joint interventions were conducted during three months.

In September 2000, there was a joint ECB-US-Japan intervention in order to stop further depreciation of the euro.

On March 18, 2011, the G7 countries intervened to reverse the direction of yen appreciation that had progressed following the Great East Japan Earthquake.

One of the proposed reasons for this appreciation was based on speculation that Japanese insurance companies would need to liquidate assets abroad and convert them to yen to pay for claims. (See Neely 2011).

The aforementioned coordinated intervention, the first since 2000, played a crucial role in stabilizing the yen.

Policy coordination on exchange rates among the G5 countries occasionally had dramatic effects during the 1970s and 1980s.

The most prominent example of this was the period bookended by the Plaza agreement of September 1985 and the Louvre accord of February 1987.

図6は、1976年から1995年まで通貨当局が介入を調整した年間月数を示しています

たとえば、1979年には、米独共同介入は9ヶ月間実施され、米独日3カ国による共同介入は、3ヶ月間実施されていることが示されています

2000年9月、さらなるユーロ安(depreciation of the euro)を阻止するためにECB、米国、日本による共同介入が行われました

2011年3月18日、G7諸国は東日本大震災後に進行した円高を反転させる(reverse the direction of yen appreciation)ために介入した実績が残っています

この円の増価(this appreciation)に対する介が提案された理由の1つは、日本の保険会社が保険金支払いのために海外の資産を清算し、円に交換する必要があるという推測に基づいているからであると言われています (ニーリー 2011を参照)

2000年以来初となる前述の「円高是正を目的とした協調介入」は円の安定(stabilizing the yen)に重要な役割を果たしたと言えるのです

G5諸国間の為替レートに関する政策調整は、1970年代と1980年代に劇的な効果をもたらすことがありました

この最も顕著な例は、1985年9月のプラザ合意と1987年2月のルーブル合意によって終了した期間でした

6.2. Case Study: Policy coordination under the Plaza and Louvre agreements

こちらのセクションは割愛させていただくことにします📝

ぜひご興味のある方は、該当リンクからご確認いただけますと幸いです💖

本日の解説は、ここまでとします

このような歴史や先行研究をしっかり理解した上で、卒業論文執筆に取り組んでいきたいです

読み終えた先行研究📚

『日本の為替介入の分析』 伊藤隆敏・著

経済研究 Vol.54 No.2 Apr. 2003

『Effects of the Bank of Japan’s intervention on yen/dollar exchange rate volatility』21 November 2004

Toshiaki Watanabe (a), Kimie Harada (b)

『The Effects of Japanese Foreign Exchange Intervention: GARCH Estimation and Change Point Detection』

Eric Hillebrand Gunther Schnabl Discussion

Paper No.6 October 2003

私の研究テーマについて🔖

私は「為替介入の実証分析」をテーマに

卒業論文を執筆しようと考えています📝

日本経済を考えたときに、為替レートによって

貿易取引や経常収支が変化したり

株や証券、債権といった金融資産の収益率が

変化したりと日本経済と為替レートとは

切っても切れない縁があるのです💝

(円💴だけに・・・)

経済ショックによって

為替レートが変化すると

その影響は私たちの生活に大きく影響します

だからこそ、為替レートの安定性を

担保するような為替介入はマクロ経済政策に

おいても非常に重要な意義を持っていると

推測しています

決して学部生が楽して執筆できる

簡単なテーマを選択しているわけでは無いと信じています

ただ、この卒業論文をやり切ることが

私の学生生活の集大成となることは事実なので

最後までコツコツと取り組んで参ります🔥

本日の解説は、以上とします📝

今後も経済学理論集ならびに

社会課題に対する経済学的視点による説明など

有意義な内容を発信できるように

努めてまいりますので

今後とも宜しくお願いします🥺

マガジンのご紹介🔔

こちらのマガジンにて

卒業論文執筆への軌跡

エッセンシャル経済学理論集、ならびに

【国際経済学🌏】の基礎理論をまとめています

今後、さらにコンテンツを拡充できるように努めて参りますので何卒よろしくお願い申し上げます📚

最後までご愛読いただき誠に有難うございました!

あくまで、私の見解や思ったことを

まとめさせていただいてますが

その点に関しまして、ご了承ください🙏

この投稿をみてくださった方が

ほんの小さな事でも学びがあった!

考え方の引き出しが増えた!

読書から学べることが多い!

などなど、プラスの収穫があったのであれば

大変嬉しく思いますし、投稿作成の冥利に尽きます!!

お気軽にコメント、いいね「スキ」💖

そして、お差し支えなければ

フォロー&シェアをお願いしたいです👍

今後とも何卒よろしくお願いいたします!

この記事が気に入ったらサポートをしてみませんか?